> For the complete documentation index, see [llms.txt](https://docs.xb3.finance/llms.txt). Markdown versions of documentation pages are available by appending `.md` to page URLs; this page is available as [Markdown](https://docs.xb3.finance/digital-asset-education/defi/defi-rewards-where-do-they-come-from.md).

# DeFi Rewards? Where do they come from?

## Intro

When you first step into the world of DeFi, you are presented with information that seems unfathomable at first. You might be overwhelmed, as everything you are seeing and learning about seems quite far from the norm. In a traditional legacy system, people seem to feel at ease with the fact that other entities have control over your funds while you earn a staggering 0.1%, if that, on your capital. What if I told you that that wouldn't have to be the case with you... \

\

I am sure by now that you have heard of the much higher yields that people achieve in DeFi and the intricate technology behind it, and it is my job to ensure that you have a deep understanding of how these yields are generated so that you as an individual can have complete control over your funds and deploy your capital as you please.

Before we get into the first stream of DeFi rewards, it is imperative that you understand the history behind the DeFi protocols and the initiatives that they have taken to get us where we are today. The emergence of Decentralised Finance protocols has been ever-expanding and has allowed users to tap into highly liquid and interoperable financial services. Before the inception of Decentralised Exchange (DEX) projects like Uniswap, volume trading in the Traditional Legacy system or Centralised Exchanges was based on the order book model in which buyers and sellers meet at an equilibrium price - buyers try to buy at the lowest possible price and sellers try to sell at the highest. Market makers came into play to facilitate trading on demand by always being willing to buy or sell a particular asset - which they do by providing liquidity of both assets to the market in the form of standing trade orders. This narrative of a centralised exchange brings a few complexities along with it such as the fact that funds held at a centralised exchange are kept in accounts where they control the private keys, meaning you have to trust them to hand over ownership of your funds when you ask for it. Because these centralised entities literally control all funds, they act as an intermediary - which is generally a regulated financial services role that restricts people from certain jurisdictions from using their services. These complexities fall away with decentralisation as it minimises the need to trust and rely on a central authority for governance. DeFi provided a plethora of opportunities to achieve a transparent and robust financial system that no single entity controls. With this decentralisation in mind, it leads us to an entirely new way of trading that emerged only recently, Decentralised Exchanges (Dexes). Dexes utilize blockchain technology and are part of the growing suite of decentralised finance tools that makes a huge range of financial services available directly to users who can participate from non-custodial (not being held on your behalf by someone else) cryptocurrency wallets.

Uniswap is a leading decentralised exchange that allows for the swapping of tokens without the necessary counterparty (i.e. buyers and sellers) that you would expect in an order book based trading platform. Rather, Uniswap allows users to buy or sell a particular asset by interacting with a liquidity pool through an automated market maker (AMM). In its basic form, liquidity pools hold two token assets in equal measure and these pools of tokens sit inside of smart contracts that are again, used to facilitate trading. Instead of an order book system where the price of each asset is determined by the highest buyer and lowest seller, the automated market maker (AMM) system completes trades for users on demand. This revolutionary method for adjusting the price of an asset based on its supply and demand uses a well known mathematical equation that give these type of “Constant Product Market Maker” Dexes their names - the Constant Product Formula:\

\

**x \* y = k.**\

\

It works by increasing and decreasing the price of one asset depending on the ratio of how many tokens there are proportional to the other token in the liquidity pool. We will unpack this mathematical formula below as it will benefit us in understanding where the first stream of DeFi rewards come from.

The mathematical formula mentioned above brings to light the endless possibilities of yield in DeFi and has also paved the way for other Dexes to modify it to suit their objectives (this will be unpacked under the “Curve” section). As we mentioned before, these liquidity pools use a mathematical formula: x \* y = k where ‘x’ and ‘y’ are the quantity of coins in the liquidity pool and ‘k’ is a constant product, meaning that it is a value that cannot change.

In mathematical terms, the formula states that trades must not change the product (k) of a pair’s reserve balances (x and y), and therefore whenever you make a trade and “pay” (by adding your input asset to the pool) to “buy” (which takes your output asset out of the pool) you change the ratio between the two assets, and the constant product formula ensures that the “rate” or price that you pay for the one is inflated enough so that the product “k” remains the same after the trade. In simple terms, you end up paying proportionally more for each token the larger your trade size (called price slippage) in order to incentivize price equilibrium between the tokens

In a similar fashion, the only way to add funds to the pool that would NOT change the ratio of tokens would be to provide both assets at the current proportional ratio (e.g. $1000 of ETH & $1000 of XB3). Adding liquidity in this way INCREASES “k” - but maintains the price ratio.

The size of ‘k’ is super important as it is essentially ‘the size of the liquidity pool’. This size will determine how much the price of tokens will change during a trade, thus, the more liquidity there is in a pool, the easier it is to make larger trades without causing the price to slide as much (ie. slippage).

Finally when you remove liquidity from a pool you can also only do so at the current ratio of assets so that the ratio between the two tokens remains the same. Removing liquidity in this way DECREASES “k” - but maintains the price ratio.

eg.

This idea of liquidity pools finally brings us to our first generation of rewards which are swap fees. As mentioned above, users can put up their liquidity to work by providing both x and y, however to incentivise this, Uniswap charges a small transaction fee of 0.3% on trades that is used to pay out liquidity providers. This means that I can provide liquidity to the pool and earn rewards from people trading in the pool since they are essentially using my liquidity to trade on. This was exceptionally beneficial for the protocol and DeFi as an entirety as users were now incentivised to provide liquidity, which in turn, reduced the slippage on transactions and caused less prominent price actions on tokens. However, the rewards did not stop there.

In order to attract even more liquidity from providers, protocols started to pay out additional incentive fees to users, mostly in their native token, as inflationary token rewards. This leads us to the second generation of rewards that protocols implemented to attract deep liquidity (sufficiently large volumes of both tokens to provide competitive trade values with low price slippage), and these are called **inflationary rewards**. Alongside the increased revenue for a liquidity provider from these, the inflationary rewards also allow providers to get a share of the Dex platform and earn not just the fees, but simultaneously allowing you to participate in new protocol products specifically designed for providers. Curve finance is a protocol that has implemented these reward mechanisms in addition to creating products for providers that amplify their yield. This enables providers who provide liquidity on Curve to receive a proportion of trading fees on their pool, as well as earning additional rewards in Curve’s native token, CRV. We will continue this story by explaining how Curve.fi has added to this ecosystem through their innovation.

## Curve

Similar to Uniswap, Curve is a decentralised exchange, however it focuses heavily on the exchange of stablecoins (USDC to DAI for example) with low fees and low slippage. For those who do not know, stablecoins are cryptocurrencies that are FIAT backed or algorithmically backed, among others. These stablecoins are pegged to another asset class, such as a FIAT currency with examples including USDT or USDC. This means one USDC/USDT has either 1 USD in the bank account, or 1 USD of representative value backing the asset - ensuring the value of each stablecoin. As stated previously, other Dexes use the mathematical formula (x \* y = k) to determine the price of a trade, however Curve fi has taken the initiative to create new mathematical formulas to power their protocol. Considering that Curve is heavily focused on the swapping of stablecoins, and that stablecoins are designed to be relatively ‘stable’, it is important that when people are trading in and out of the pool, that the stablecoins keep their peg of $1 (or as close to that as possible). To achieve this, Curve uses completely new maths and has ensured that their graph differs from the Uniswap (x \* y = k) graph. The Curve graph looks similar to the Uniswap function however it differs in the fact that it has a flattish region in the middle, which can be visually explained below:

Now a lot of this information may seem quite complex at first, but in reality it can be fairly straightforward. To summarize it, Unsiswap is essentially a decentralised exchange that focuses on the swapping of tokens. They use AMM’s and liquidity pools to facilitate trading instead of trading via the order book model. Users can provide liquidity (both x and y) and receive rewards from trading fees. The more liquidity there is in a pool, the less prominent price movements will be when large trades occur. The large amount of liquidity ensures low slippage, and where in traditional systems, slippage is what happens when traders have to settle for a different price than what they initially requested due to a movement in price between the time they did the trade and the time it was actually executed. Slippage in a DEX is determined by the price impact the size of a trade has on the pool’s remaining liquidity. Too much slippage can cost frequent traders a lot of money and is something that Curve aimed to solve. Curve focuses on the swapping of stablecoins with low fees and low slippage. Liquidity providers ensure that Dexes have sufficient liquidity to complete trades on demand, and earn trading fees - as well as potential inflationary DEX token rewards. In Curve, individual users can provide liquidity and receive trading fees as well as inflationary CRV rewards (Curves native token), which are just two of the several ways that users can earn rewards in DeFi. To build on this narrative even further, I will be doing a deep dive into Curve as well as the protocols that have built on top of them.

Curve has two main components. For the sake of the story being told we will consider them as a trade-side and a rent-side if you will. On the trade-side, users can take stablecoins to Curve and swap them for any other supported stablecoin, thus making it like a Uniswap for stablecoins. When swapping stablecoins, you will pay a small transaction fee and a rebalancing fee. The rebalancing fee is determined based on how far the pool has diverged from its configured proportions (i.e. how far the quantities of the tokens have moved from 50:50). For example if a pool is supposed to be 50% DAI and 50% USDC and the current balances are equal (i.e. 50:50), then there will be no rebalancing fee (beyond the quantity you buy). Contrary to that, if there is a disproportion in the current balances (eg. 25% DAI and 75% USDC) you will pay a rebalancing fee if you buy DAI with USDC but you will pay a negative fee (i.e. get a refund) if you buy USDC with DAI. With regards to the rent-side, users can take stablecoins to Curve and provide or ‘rent’ it to a liquidity pool to earn yield. Since stablecoins are far less volatile than other cryptocurrencies, they're perfect for liquidity providers to avoid impermanent losses. By ‘renting’ your stablecoins (liquidity) to a Curve pool, you earn yield from sources such as the transaction fees mentioned above, as well as the inflationary rewards in the form of CRV. You earn rewards pro-rata, based on your percentage share of the pool. The higher the transaction volume and the more of the pool you own the more yield you will generate. There are also some liquidity pools that will deposit the capital into DeFi lending protocols to earn additional yield. This brings us to another stream of rewards, which is lending and borrowing. Protocols like Compound and Aave allow users to supply and borrow capital whereby they can earn rewards, essentially allowing for crypto lending interest. Many Curve equivalents (stablecoin exchanges) have come and gone and have not been successful. Why Curve stands out above it’s peers is due to the conglomerate of incentives that came along with it as well as the many restriction mechanisms implemented to protect users and liquidity. Curve solved several problems by directly integrating with yield-generating DeFi protocols to provide a base level of yield. They also ensure to share all of the transaction fees with liquidity providers and in addition to that, Curve has its own token which it pays out as a reward on top of fees. This may raise the question of ‘If Curve is consistently creating more of these tokens, won’t the inflation create massive sell pressure?’ and as counter-intuitive as it sounds, it does not. Curve has implemented mechanisms in which users can lock their CRV tokens to receive veCRV (vote escrowed CRV). One of the main incentives for CRV is the ability to boost your rewards on provided liquidity. By locking your CRV for sufficient amounts of time, you receive veCRV which allows you to acquire voting power to participate in DAO proposals and pool parameters, AND it also allows you to earn a boost of up to 2.5x on the liquidity you are providing on Curve. This will be touched on again under the “Convex” section. The inception of Curve finance has driven massive growth in the market caps of stablecoins and has allowed for amplified yield, while simultaneously taking advantage of the low fees and slippage. Curve has set a solid foundation for future protocols and the endless possibility of complementary yield, which brings us to our next point, Convex.

## Convex

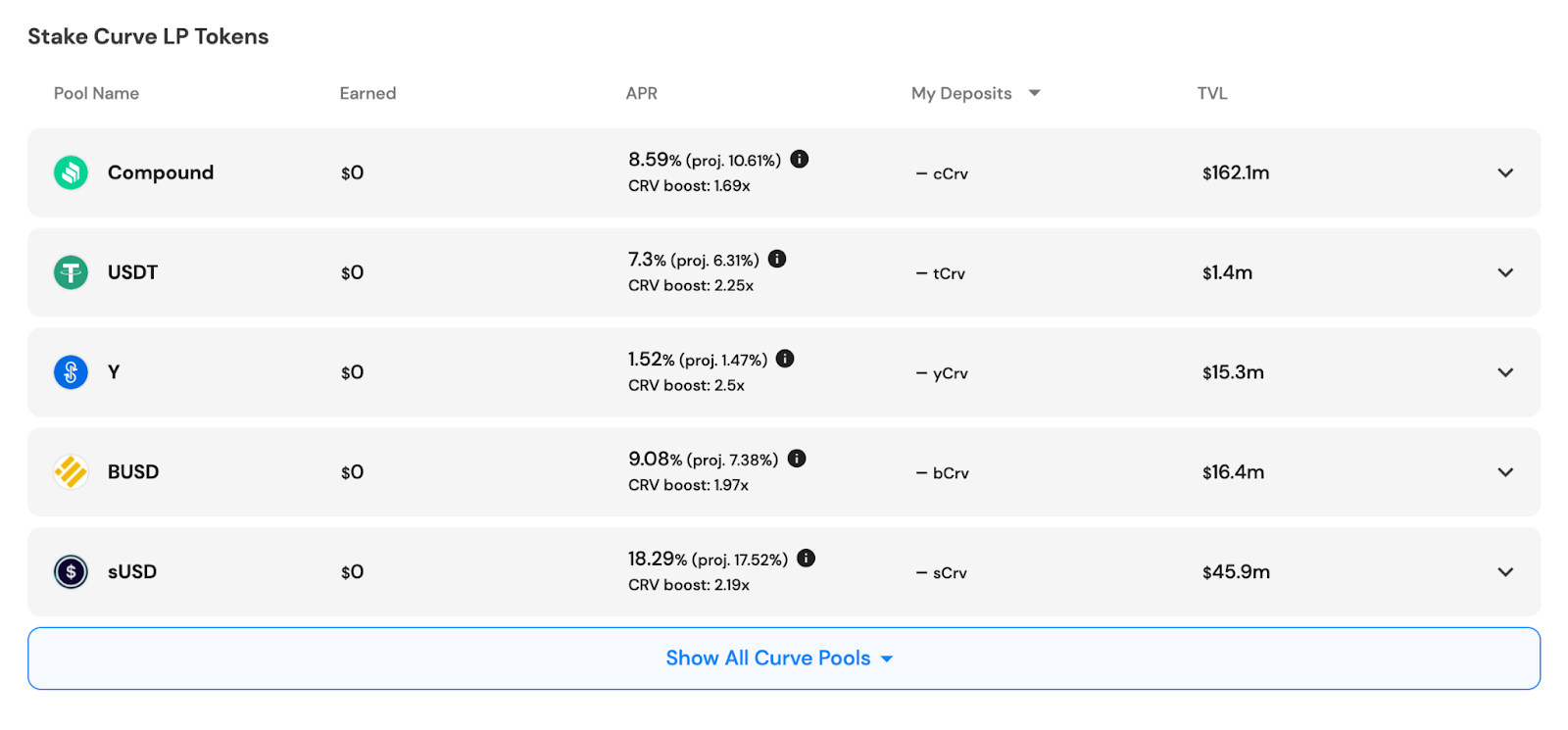

Convex Finance is a platform for CRV token holders and Curve liquidity providers to earn additional rewards and Curve trading fees on their tokens. In its simplest form, Convex finance boosts Curve staking rewards. Users can deposit their Curve LP tokens through Convex who deposits this back into Curve to further amplify yield. Think of Convex as the second LEGO piece in a 3 story tower, with Curve being the foundation. To understand how Convex works, we have to remind ourselves of how Curve works. Curve liquidity providers are rewarded in transaction fees as well as inflationary CRV rewards. CRV rewards are convertible into veCRV (by locking CRV). veCRV can be used in governance, boosting rewards, earning trading fees, and receiving airdrops. The more veCRV you have, the more you can boost the CRV rewards from your liquidity pool. You can boost your CRV rewards as high as 2.5x if you apply the maximum amount of veCRV required for your deposited liquidity. Subsequently, the more liquidity you provide in the pool, the more veCRV is required to boost your returns up to the maximum of 2.5x. So, to get maximum rewards would require a lot of veCRV, especially if you are a large liquidity provider... Now that you have an understanding of the fundamentals, we can look even deeper and start to appreciate the intricate economics behind it. Curve users are incentivised to provide liquidity as they receive rewards from trading fees and the inflationary CRV rewards. To incentivise users even more, they are able to lock their CRV tokens to receive veCRV and in doing so, are able to boost CRV rewards by up to 2.5x on provided liquidity. This locking mechanism drastically changes the game as now there are restrictions on circulating supply of CRV - which reduces the possible sell pressure at any given point in time. \*insert infographic (Alice LP’s -> receives rewards -> locks CRV for veCRV, applies veCRV to LP -> receives up to 2.5x) So what is Convex doing differently and how are they doing it so well? Convex is essentially pooling their assets together so the platform can acquire more CRV, convert it into veCRV, and in turn maximise the boost to all Curve liquidity providers. Regardless of the size of your liquidity provider (staking) position, Convex usually lets you get a better reward boost out of them than by entering Curve directly as a new user. It is imperative to note that not all Convex pools are boosted to the max. Boost is pooled by CRV stakers so some pools are sitting at 1.69x, while others are at 2.5x (as seen in the screenshot below). What makes some pools boosted higher than others is the amount of veCRV applied to the pool. This application of veCRV to pools benefits all liquidity providers through Convex as you are no longer needed to acquire veCRV for boosted rewards - so both small and large LP’s can immediately get better returns.

So why would one deploy their capital into Convex you might ask? Well, the simple answer is that there are more rewards. As a liquidity provider on Curve who has staked my LP tokens through Convex, I would receive rewards from the base rate return (on Curve), plus my proportion of Curve trading fees, plus my boosted CRV rewards (from Convex), and finally add additional rewards in Convex’s native token, CVX.

\

Because of this yield enhancement, Convex caught a lot of attention and has been steadily gaining more popularity ever since. At the time of this writing, Convex currently has a TVL (total value locked) of \~5 billion dollars. DeFi users rushed into the idea of ‘boosted rewards’ which has further helped Convex on its journey of complementary yield. This narrative has helped develop other protocols to focus on similar initiatives.

---

# Agent Instructions

This documentation is published with GitBook. GitBook is the documentation platform designed so that both humans and AI agents can read, navigate, and reason over technical content effectively. Learn more at gitbook.com.

## Querying This Documentation

If you need additional information that is not directly available in this page, you can query the documentation dynamically by asking a question.

Perform an HTTP GET request on the current page URL with the `ask` query parameter, and the optional `goal` query parameter:

```

GET https://docs.xb3.finance/digital-asset-education/defi/defi-rewards-where-do-they-come-from.md?ask=&goal=

```

`ask` is the immediate question: it should be specific, self-contained, and written in natural language.

`goal` is optional and describes the broader end goal you are ultimately trying to accomplish on behalf of the user. GitBook uses it to tailor the answer towards what is most useful for that goal.

The response will contain a direct answer to the question and relevant excerpts and sources from the documentation.

Use this mechanism when the answer is not explicitly present in the current page, you need clarification or additional context, or you want to retrieve related documentation sections.